When it comes to financial planning, the simplest questions can have the most profound answers.

· Am I saving enough?

· When can I retire?

· Am I on the “right track”?

These questions, although simple, can feel overwhelming to answer. People may try to consider every possible scenario and every possible factor until they are left with more questions and more anxiety. If no one is focused on addressing these questions, then that anxiety is justified. The financial unknown has great depth.

But these questions do have answers. As a matter of fact, you have the answers. It all comes back to how you want to spend.

Financial planning should create a continuity to your financial lifestyle.

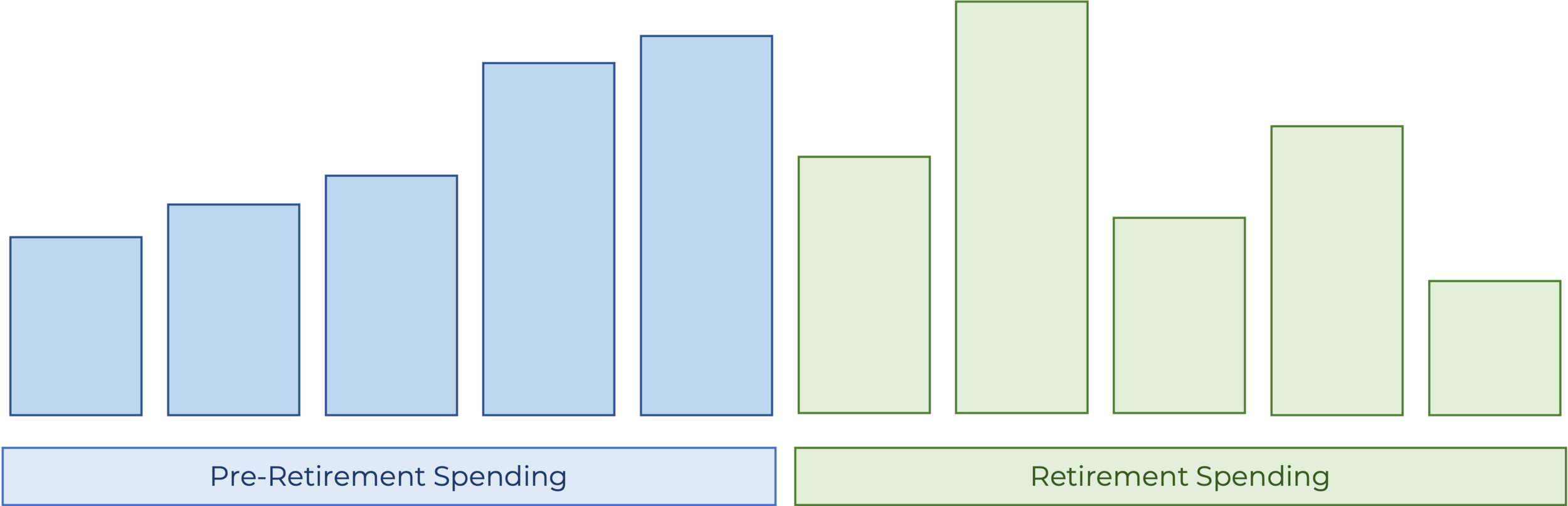

This is a simple illustration that shows a seamless transition from pre-retirement spending to post-retirement spending. The financial plan has not saved too much nor too little. The spending is steady and is benchmarked from the client’s highest spending years prior to retirement. This spending continues until a predictable decline later in life (most 85-year-old retirees spend less than 60-year-old retirees).

Saving too much for your future retirement is a sacrifice made today.

Saving is a positive habit. We are taught early on that delayed gratification is a cornerstone of a healthy financial life. We choose not to spend today so that we can spend more later. We will eliminate the consideration completely by automating our 401(k) contributions or other savings.

However, savings is a sacrifice and can be unnecessary. We rarely ask ourselves what we are saving for? Is it possible I am saving too much? To answer these questions, we again must turn to our spending.

This illustration shows a financial plan that has saved too much. There has been too much saving prior to retirement and, as a result, can afford far more spending in the retirement years. This sounds like a financial victory, but who wants to wait until his/her 60s to enjoy the one financial life we have? Why eat canned tuna fish now and caviar later?

Not knowing how much to save is a big problem.

This is the problem that people are most afraid of and rightfully so. This financial plan has not saved enough for retirement. The financial lifestyle that was once enjoyed is now unsustainable. This could have stemmed from lifestyle creep – allowing spending to increase in an uncontrollable way. Or this could be a result of simply not knowing how your spending would change as a result of retiring earlier.

In either case, this is the most difficult adjustment to make. Once you retire, it is very difficult to go back to work. Once you are accustomed to a certain financial lifestyle, it is very difficult to reduce your spending. This financial plan went from caviar to canned tuna fish.

Your financial lifestyle is not solved by a rule-of-thumb – safe withdrawal rate strategies.

People often believe that they just need to have a certain dollar amount saved in order to retire comfortably. They may have heard that one can withdrawal a fixed percentage of their portfolio each year to minimize the risk of running out of money early. Sure, you may not run out of money, but your spending would be determined by your portfolio value. The value of your portfolio, in turn, is determined by the irrational behavior of the financial markets. The graph above illustrates that you may be able to spend more in some years and less in other years. No one wants to decide if they can live their ideal financial lifestyle based on how the financial markets perform each year.

Your financial lifestyle is determined by you.

Every financial plan and every financial lifestyle is unique. It is up to you how you want to live your financial life. Some may want to ease into retirement by working less (shown above), others want to spend as much as they can, or others may want to spend less so others can have more. It is your spending that determines how much you should save, what your allocation should be, or when you can retire. Your goals should be the driving factor in all of your financial decisions. Having an understanding of your spending will answer many of these seemingly “difficult” questions.